Unlocking the Upstream Advantage: OpenVault’s Insights for ISPs

- David Gray

- Apr 8

- 5 min read

Last week the Fiber Broadband Association presented “Capacity, Competition & Cash Flow: The Upstream Equation,” moderated by FBA President Gary Bolton. It was a panel discussion with Mark Trudeau, Founder and CEO of OpenVault, and Jeff Heynen, Vice President of Broadband Access and Home Networking at Dell’Oro Group. The conversation unpacked OpenVault’s latest 4Q 2025 Broadband Insights report (OVBI), “Unlocking the Full Power of Upstream,” and offered a clear view of how consumer behavior is evolving based on speed capabilities and new applications.

Trudeau’s perspective is clear: downstream speed isn’t the whole story anymore. Upstream, latency and how speed tiers are actually used are now central to product, planning and competitive strategy—especially for small and regional ISPs.

OpenVault’s vantage point

OVBI isn’t a survey; it’s based on actual traffic from millions of subscribers, anonymized and analyzed via OpenVault’s cloud platform. That gives a broad, operator‑agnostic view into how usage is evolving on both DOCSIS and fiber networks.

Three findings from the 4Q25 report matter most for regional ISPs:

Upstream usage is growing much faster than downstream.

Fiber and DOCSIS subscribers behave very differently when upstream capacity changes.

Speed‑tier adoption has consolidated into a few “real” tiers, with important differences between fiber and DOCSIS mixes.

Upstream in the spotlight

OpenVault’s year‑over‑year comparisons show that total and downstream usage are still growing steadily, but upstream has broken out.

Total usage: +9.9% YoY.

Downstream usage: +9.1% YoY.

Upstream usage: +21.7% YoY.

Median usage growth re‑accelerated to +15.3%, almost as much as the prior two years combined.

This all makes good sense in a world where work‑from‑home, cloud collaboration, social video, gaming and AI tools all lean on the return path. The question for operators is no longer “Can my customers stream Netflix?” It’s “Can three or four people do upstream‑intensive things at the same time without diminishing the experience?”

"Most households are now content creators"

Jeff Heynen observed that this matches what he hears from operators: upstream has become a real point of differentiation – not just a technical specification.

Both Mark and Jeff cited a noteworthy example that emerged in a panel discussion during the Cable Next‑Gen Technologies & Strategies 2026 conference in late March in Denver. A cable operator presented the significant network impact from OpenAI’s Sora video generation tool. Importantly, Sora is not currently widely available – users needed an invitation in order to access. Despite this constraint, AI traffic surged so much that Sora accounted for about 2% of AI-related upstream traffic. Once the operator disabled Sora, the video percentage of AI traffic dropped to 0.3%. So, in a very short window, with a highly constrained base of users Sora became a very noticeable slice of AI-related traffic.

The takeaway here is that most households are content creators at this point, whether it’s TikTok, Twitch, or text-to-video tools. It’s a preview of what happens when new creator tools—AI video, richer social platforms, real‑time collaboration—move from pilots into the mainstream. The OVBI numbers suggest that if you give those households more upstream headroom, they will use it.

Like‑for‑like behavior: fiber vs DOCSIS on the same operator

The most interesting OVBI finding, in my view, is an apples‑to‑apples comparison between fiber and DOCSIS subscribers on the same network operator, in the same market. In this example:

Fiber subscribers are on a symmetric 677 Mbps service.

DOCSIS subscribers average about 17.3 Mbps upstream on their tiers.

OpenVault found that:

DOCSIS subs used about 56 GB of upstream per month.

Fiber subs used about 93 GB—roughly 66% more upstream usage.

Figure 1: Dec 2025: Fiber vs DOCSIS Upstream Usage (GB), 4Q OVBI

The takeaway isn’t simply that “fiber users are heavier users." It’s that when upstream capacity is readily available, consumers change their behavior. Users don’t worry about whether the upload will bog down a video call, or whether their kids’ gaming will ruin a Teams meeting. They just use the connection the way modern life demands.

Jeff’sobservation was that this matches what operators see when they complete mid‑split or high‑split upgrades: once upstream bottlenecks are relieved, utilization typically ramps quickly. From a strategy standpoint, that means upstream upgrades buy you more than marketing headlines—they unlock latent demand.

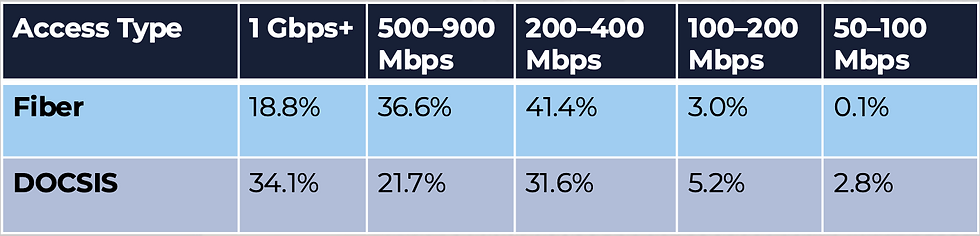

Speed tiers: consolidation and different roles for fiber vs DOCSIS

OVBI also takes a close look at speed‑tier distribution. A few points stand out:

87% of subscribers are now provisioned at 200 Mbps or more.

The 200–400 Mbps tier grew from 21.2% to 31.6% of subs in a year—a 49.1% jump.

1 Gbps+ penetration was roughly flat, nudging from 34.8% to 34.1%, while several lower and mid‑range tiers shrank.

OpenVault then splits this by access type:

On fiber, 41.4% of subs are at 200–400 Mbps and 36.6% at 500–900 Mbps; only 18.8% are at 1 Gbps+.

On DOCSIS, 34.1% of subs are at 1 Gbps+, with fewer in those mid‑range tiers than on fiber.

Figure 2: Speed Tier Distribution by Access Type, 4Q OVBI

OpenVault’s explanation is fairly intuitive. On DOCSIS, moving to a gigabit tier often delivers a meaningful upstream bump, so households with rising upload needs jump there even if they don’t really need 1 Gbps down. On fiber, symmetry is the default; a 300 or 500 Mbps tier already provides strong upstream, so fewer people feel compelled to pay for gigabit.

The larger lesson is that speed‑tier adoption is no longer a reliable proxy for usage intensity or network stress. Flat gigabit penetration does not mean demand has plateaued. It may simply mean subscribers are finding what they need in mid‑range symmetric tiers while still pushing more traffic through them—especially upstream.

Implications for small and regional ISPs

If you’re running a 10k–250k‑sub network, especially in mixed‑technology markets, here’s how I’d translate these findings.

Make upstream and latency front‑and‑center in your product

OpenVault forecasts that upstream is where the next crunch will be, so what are the implications?

HFC operators: a clear mid‑split/high‑split roadmap, plus upstream noise management and profile optimization, is now table stakes if you expect to compete with FTTH for households that are already behaving like content creators.

FTTH operators: symmetry is your most under‑used differentiator. Sell “creator‑grade uploads,” “Zoom that just works” and “AI‑era connectivity,” not simply “fiber is faster.”

Design your speed ladder around 200–400 Mbps and gigabit service with a purpose

OVBI’s speed‑tier data offers a useful guide rail:

Make 200–400 Mbps your core residential tier; that’s where the market is already migrating.

Treat gigabit‑plus as a premium with a reason: visibly better upstream and lower latency under load, possibly bundled with enhanced gig-capable Wi‑Fi or proactive monitoring—not just a bigger number on a web page.

Quietly retire or de‑emphasize your sub‑100 Mbps tiers wherever you can; they don’t match real usage and they’re easy for “good enough” alternatives to pick off.

As you plan, talk in gigabytes, not just percentages

When you’re developing budgets, or talking with your board, frame growth in terms of additional gigabytes needed per household per year -- with upstream rising fastest -- not just “we’re growing 9 - 10% each year”. The implications of the OpenVault report are pretty clear: the future of broadband competition will be defined less by who can tout the biggest downstream number, and more by who can consistently deliver reliable, bi‑directional performance for households that are increasingly creators as much as consumers. For small and regional ISPs, that’s actually good news. You don’t need a national footprint to get upstream and product strategy right—you just need a clear view of how your customers are really using your network and a plan to stay a step ahead of them

Comments